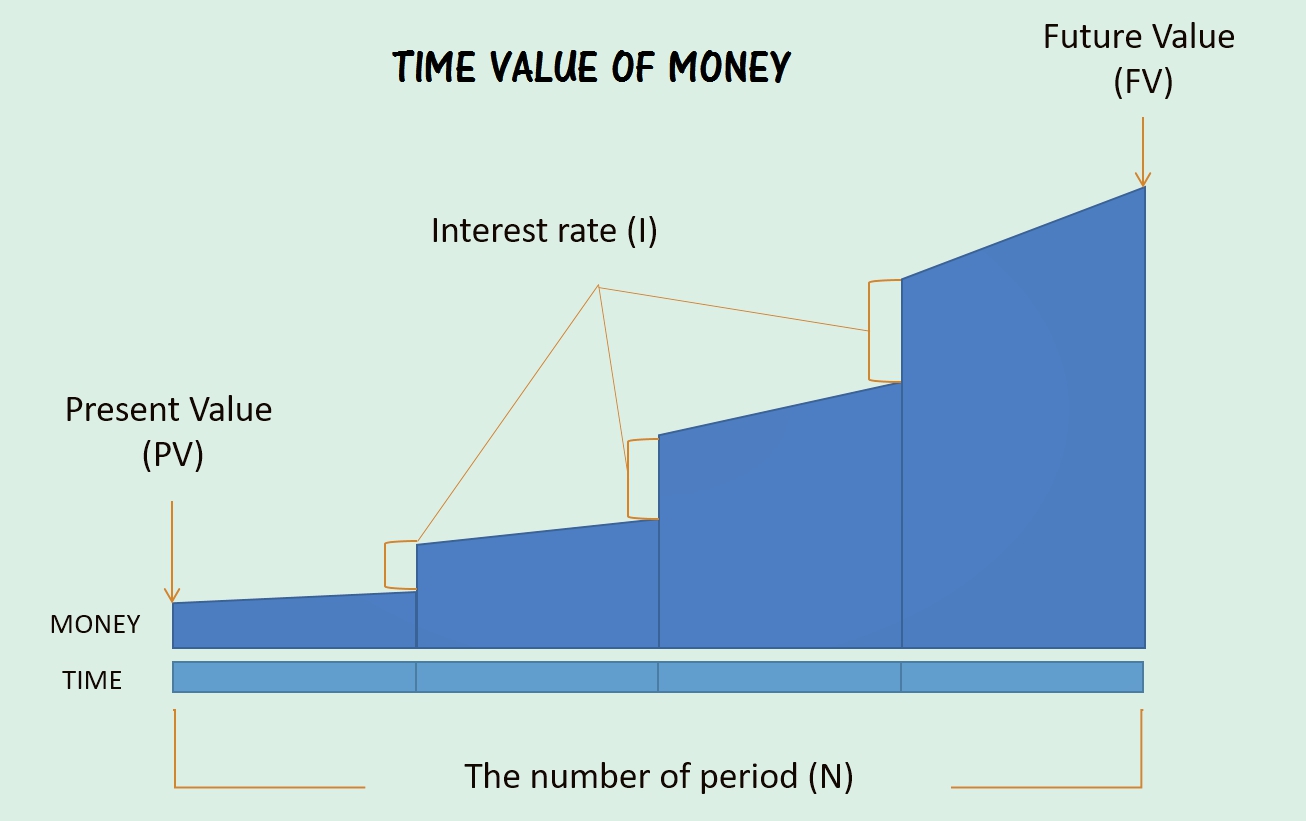

The concept of time value money (TVM) asserts that the value of money (or a dollar) today is worth more than the value of a dollar in the future. Under normal inflation conditions, money today is worth more than the same amount in the future. Inflation increases prices over time, such that the amount of money you have today will buy more now than it will in the future.

Additionally, the time value of money also involves an opportunity cost. For example, if you put $ 5000 in a savings account to save for a car, you will be giving up an opportunity to grow that money in an investment account.

The Future Value (FV) and Present Value (PV) can be calculated using Financial Calculators or financial formulas found in the Excel worksheets/spreadsheets. The Excel financial formulas can also be applied in the Open Office suite or Google Docs & Spreadsheets.

Where:FV=Future ValuePV=Present Valuen=Number of periodsr=Rate of return or Interest rate or Discount rate or growth per period

Compound Interest

The interest rate in the above formulas is compounded at certain intervals of time. This interval of time is normally assumed to be one year. However, in many cases, it is usually less than 1 year. Where the time interval is less than one year, two adjustments must be made to the formulas:

The number of times is changed to represent the number of times that interest is compounded. This is done by multiplying the number of years by the number of compounding periods within a year.

The interest rate is changed to reflect the interest rate per period. This is done by dividing the annual interest rate by the number of compounding in a year.

For example, suppose you put KES 50,000 in a savings account that pays 10% interest annually,but is compounded daily, how much will be in the account after 20 years?PV=KES 50,000 ; r= 0.10/365; and n=20 x 365

FV=PV x (1+r) ⁿ = 50,000 x (1 + 0.10/365) ⁽²⁰ ˣ ³⁶⁵⁾ = KES 369,351.62

Excel as a Financial Calculator

Excel (and other spreadsheets) is one of the most powerful financial calculators available. It provides a one-stop shop for different formulas. In the following examples, we will use Excel financial functions to solve Time Value of Money problems.

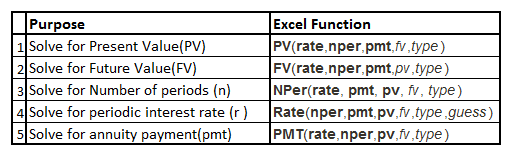

Summary /Background to Financial Calculator Keys

Like Financial calculators, Excel’s basic time value functions have five financial keys. The table below shows some of the Excel functions used in solving Time Value of Money problems.

To solve Time Value of Money problems, you have to supply at least three(3) of the arguments to each Excel function.

NB: The "bold"functions argument must be provided, while those in italics are optional.

The good thing with Excel is that you do not have to memorize the order of the arguments. You use the ‘insert function dialog box’, which then prompts you for the argument by name. You can also type the function directly and Excel will display a smart tag that shows the order of the arguments.

In the following examples, we will use Excel financial functions to solve Time Value of Money problems:

10 Easy-to-Understand Examples of Time Value of Money

Example 1:Future Value

Suppose that you want to invest $ 5,000 for a period of 5 years at an an interest rate of 8% per year. How much will you have accumulated at the end of this time period?

To solve this problem, we will use the FV function to find the future value of this lump sum investment. It is defined by the financial formula [FV (rate, nper, pmt, pv, type)].

Where,FV=Future ValueRate=Interest rate per periodNper =Total number of payment periods per in the investmentPmt=Payment made in each periodPV=The present value or the lump-sum amount that a series of future payments is worth now.Type=Value representing the timing of payment.Payment at the beginning of the period=1; payment at the end of the period =0

As you can see in the Excel worksheet below, you will have accumulated $ 7,346.64 after 5 years.

Solving for Future Value

Open a new workbook and enter the data as shown above, but leave C9 blank. Follow the step-by-step process here and see if you will get $ 7,346.64.

Example 2:Present Value

Suppose that you are planning to send your son to college in 16 years and you have determined you will need $ 120,000 at that time in order to pay for tuition & other supplies. If you believe

that you can earn an average annual rate of return of 9 % per year, how much money would you need to invest today as a lump sum to achieve your goal?

To solve this problem, we will use the PV function [PV(rate, nper, pmt, fv, type)] as shown below:

Solving for Present Value

As per the above calculation, you will need to invest a lump sum of $ 30,224.37 today to achieve $120,000 in 16 years at an annual return of 9%. If you want to reduce the initial investment amount, you will have to take more risk to earn a higher return. For example, if your return is 12%, your investment will decrease to $ 19,574.60.

NB: Time Value of Money problems have either 4 or 5 financial variables, and you are normally given 3 or 4 ,and asked to solve for the others. In this case, we are given a 5-variable problem,

are given 3 of them (rate, nper & FV), and had to solve for the fourth (PV) .You should set the

variables not in the problem to zero, otherwise they will be included in the calculation.

Example 3: Solving for the Number of Periods

Suppose that you have $ 7,500 today and you would like to know how long it will take you to

triple your money to $ 22,500. Assuming that you can earn 12% per year on your investment (after inflation adjustments),How long will it take to triple your investment?

We will use the NPer function [NPer(rate, pmt, pv, fv, type)].

From our calculations below, it will take you 9.69 years to triple your money.

Number of Periods

Remember that you have enter cash outflows as negatives and cash inflows as positives; otherwise,

you will get a #NUM error instead of the answer. If both numbers are positive, excel assumes you are getting a benefit without any investment.

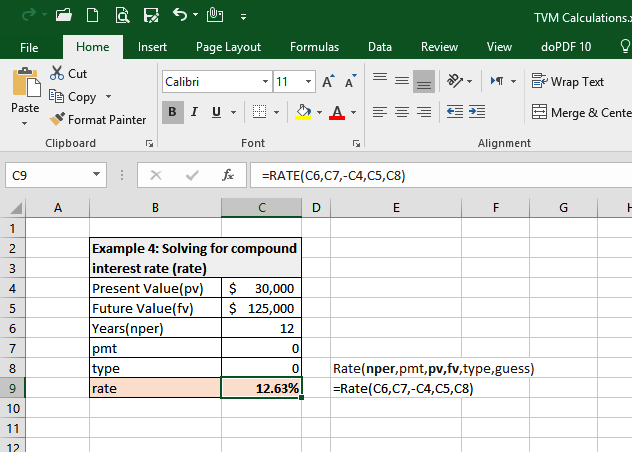

Example 4: Solving for the Interest Rate

Your friend is planning to send her daughter to college in 12 years. She has determined that she will need $ 125,000 at that time to pay for tuition & other supplies. She has $ 30,000 to invest

today.What compound average annual rate of return will she need in order to reach her goal?

We will use the Rate function; [Rate(nper, pmt, pv, fv, type, guess)] to solve this problem.

Solving for Compound interest rate

From the above calculations, if your friend is to reach her goal of $125,000 in 12 years, she will need to earn a return of 12.63% if she invests $ 30,000 today.

ANNUITIES

Annuities refer to a series of equal payments made at regular intervals such as weekly, monthly, or yearly.

The cash flow may occur at the end of the first period ( regular annuity) or at the beginning of the period(an annuity due). When using the Time Value of Money functions, omit the type of argument or set it to 0 for regular annuities. For annuity due, set the type of argument to 1.

Regular Annuity Examples

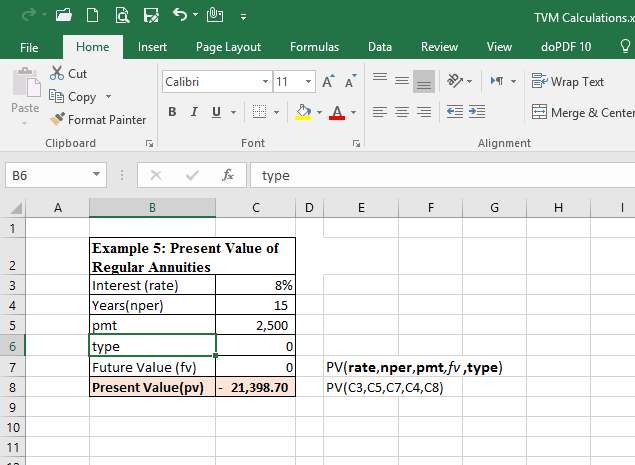

Example 5: Solving for Present Value of Annuities

Your friend informs you that an investment company offered her an investment that will pay her $ 2,500 per year for 15 years. If she can earn a rate of 8% per year on similar investments, how much should she be willing to pay for this annuity?

In this problem, you are looking for the amount your friend should pay today, so you need to solve for the present value of this annuity

We will therefore use the PV function to calculate the PV of regular annuities; [PV(rate,nper,pmt,fv, type)].

Present Value of Regular Annuities

From the Excel calculations. your friend will have to pay $ 21,398.70 today to purchase this annuity. It is negative because it is a cash outflow. The annuity payment is entered as a positive because your friend will be receiving this amount annually (cash inflow).

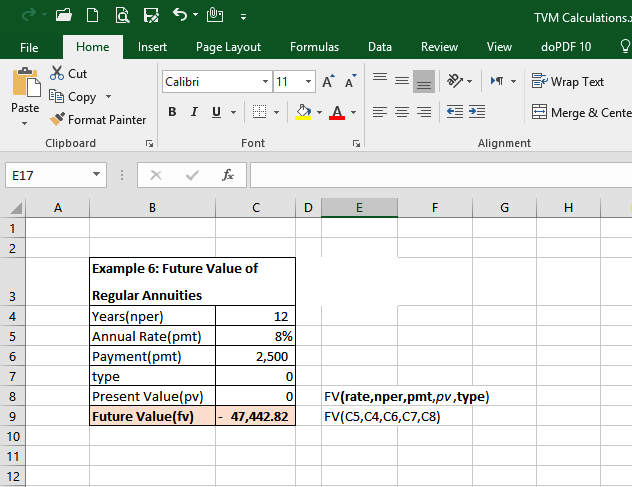

Example 6: Solving for Future Value of Annuities

Suppose that your friend informs you that she will be borrowing $ 2,500 each year for 12 years at a rate of 8%,and then paying back the loan immediately after receiving the last payment. How much will she have to repay?

In this problem, you will need to use the FV function [FV(rate,nper,pmt,pv, type) ] as shown below:

Future Value of Regular Annuities

From the above calculations, your friend will have to repay $47,442.82 after 12 years.

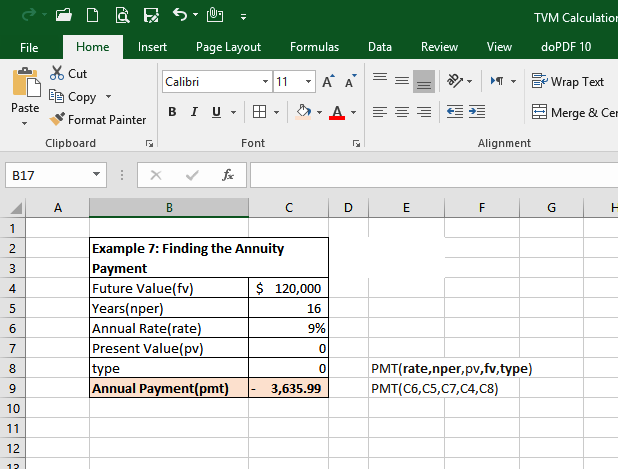

Example 7:Solving for the Payment Amount

In the last example about sending your son to school(Example 2), we determined that if you needed $120,000 for tuition in 16 years, you will have to make a lump sum investment of $ 30,224.37 at 9% per year return. This is a lot of money to invest at once.Now suppose that instead of a lump sum investment, you can invest at the end of each year.

How much will you need to invest to reach your goal?

In this problem, you will need to use the PMT. function[PMT(rate,nper,pv,fv, type)] to find the solution as shown below:

Annuity Payments

After solving for PMT, you will find that you will need to invest $3,635.99 per year for the next 16 years to meet your goal of $120,000.This is more affordable than having to raise $30,224.37 as a lump sum investment.

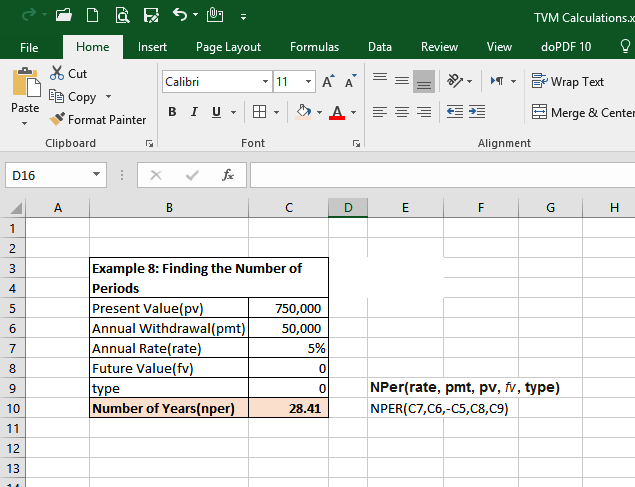

Example 8 — Solving for the Number of Periods

Suppose that you have saved $750,000 for your retirement and you expect to withdraw $ 50,000 per year. Assuming you can earn a return of 5 % per year, how long can you afford to live on this

amount?

In this problem, you will need to use the NPer function [NPer(rate, pmt, pv, fv, type)] as shown below:

Number of Periods

As you can see from the above solution, you will be able to make 28.41 withdrawals before exhausting your savings.

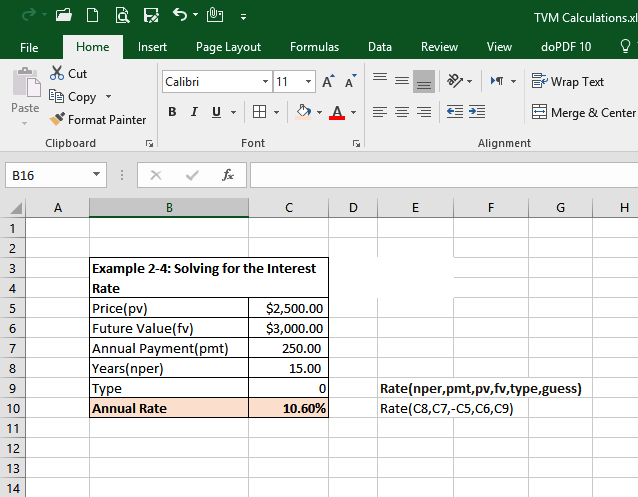

Example 9: Solving for the Interest Rate

Suppose that your friend is offered an investment that will cost $ 2,500 and will pay her an interest of $ 250 per year for the next 15 years. Furthermore, at the end of the 15 years,the investment will pay her $ 3,000. If she purchases this investment, what is her compound average annual rate of return?.

In this problem, you will need to use the RATE function [Rate(nper,pmt,pv,fv,type, guess)] as shown below:

Annual Interest rate

From the above solution, you will find your friend’s investment will earn an average return of 10.60%.

ANNUITY DUE EXAMPLES

In an annuity due, payments (or receipts) are made on the first day instead of at the end of the year/period. When solving annuity-due problems, the process is the same except that instead of inputting 0 for type, you input 1.

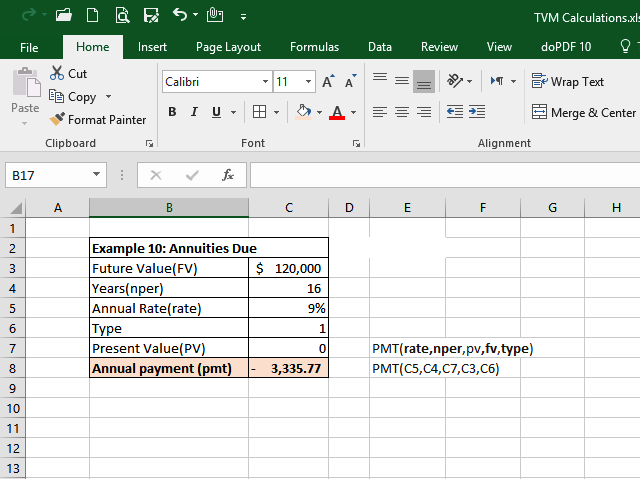

Example 10: Annuities Due

Using the same example above(Example 7)Suppose your friend is planning to send her daughter to college in 16 years. She has determined that she will need $ 120,000 at that time to pay for tuition & other supplies. She believes that she can earn an average annual return of 9 % per year. How much money will she need to invest at the beginning of each year (starting today) to achieve her goal?

Annuities due(Annual Payments)

As you can see, if your friend makes the first payment today, she will need to invest $ 3,335.77.This is about $ 300 per year less than if she makes the first payment a year from today. Investing at the beginning of the period gives her investment extra time to compound.

The Time Value of Money concept is very important to investors and is essential to anyone involved in financial decision-making processes including:

The loan amount and Equated Monthly Installment (EMI)calculations

Annuity Calculations

Insurance premium calculations, etc.

Are you revising for ATD or CPA ?

Revision4exams.com is an online platform with thousands of kasneb exams revision questions and answers.

Time value of money

Time value of money

Time value of money

Time value of money

Time value of money Time value of money Time value of money Time value of money Time value of moneyTime value of money Time value of money Time value of money Time value of money Time value of money